How is Crypto Interest Taxed? An Intro to Crypto Interest Taxes

While the new age of digital assets brings opportunity, it also brings its fair share of tax headaches. However, we’ve got you covered with a simple breakdown of how interest earned on crypto is taxed.

Unlike tax paid from buying and selling assets where your taxable amount is the price you sold it at minus the price you purchased plus a whole lot more intricacies – the amount you pay on interest earned from savings is much simpler, in the form of income tax.

And the same goes for crypto interest as the mechanics are exactly the same as your bank! Like a bank where your deposits get lent out to borrowers and your interest earned is your share of the interest they’ve paid to borrow – crypto savings works the same as your assets are trustlessly lent to borrowers with the magic of smart contracts. We’re talking about tax though and it’s a long subject so if you want to learn more we have another article covering how interest works and where does it come from?

Income Tax

The government imposes income tax on businesses and individuals by the government for earning money within their jurisdiction. Every year individuals and companies must fulfil their tax obligations and pay their taxes.

You can earn income in multiple ways, while the traditional way is through your job or labour another common way is the income you earn from putting your money to work – otherwise known as interest.

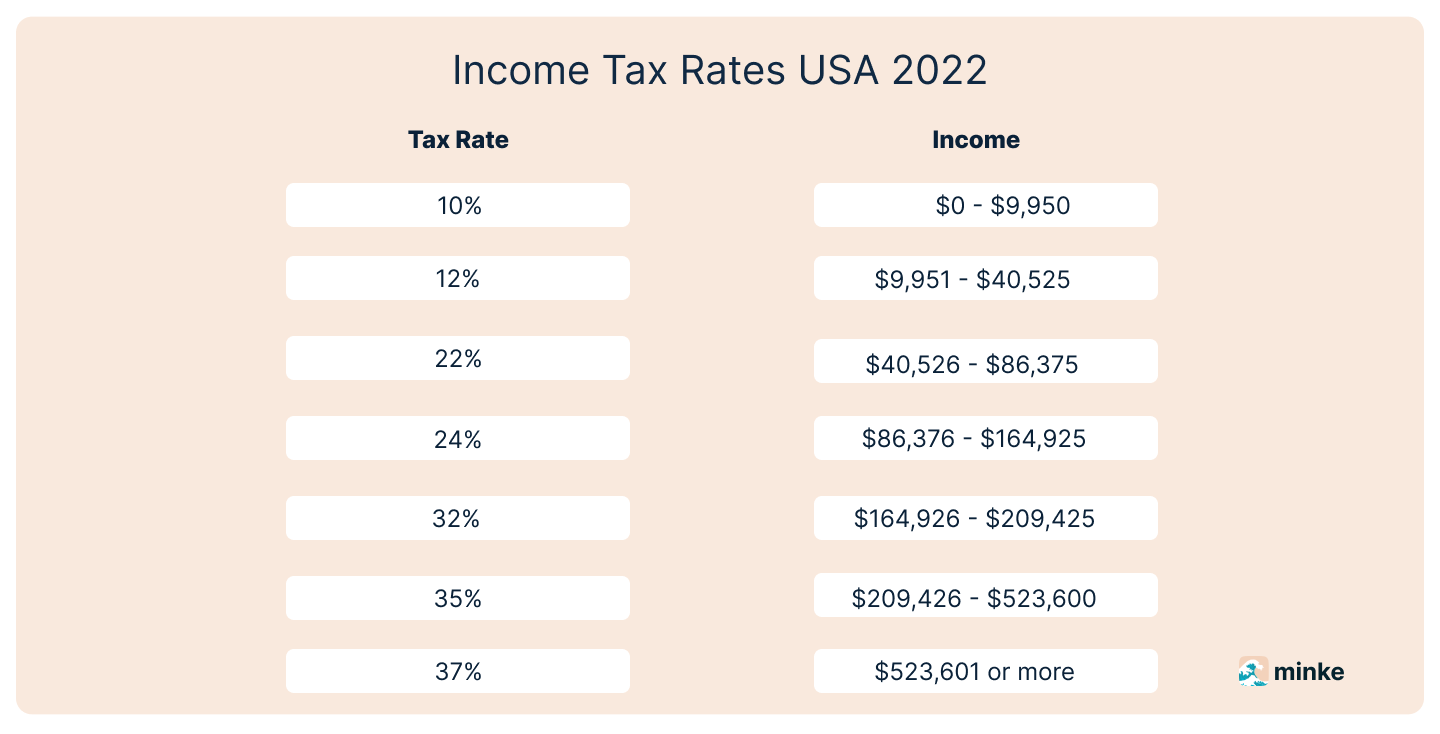

The income tax that is charged is determined by the amount of income an individual generates; thus, the higher the payment, the higher the tax, the brackets are determined by your government every year. Here are the breakdowns for 2022 in the USA:

Tools to track your taxes.

The near mainstream adoption of crypto in recent years has led to governments treating tax obligations on crypto more serious. Thus keeping a well-documented list of transactions from buying and selling cryptocurrencies as well as the interest earned from saving and staking is becoming increasingly important.

Fortunately, as adoption has grown so has the number of excellent options for tax tracking software, helping people automate the tax process and work out each individuals’ tax obligations; here are some of the top tools available today:

CryptoTaxCalculator

CryptoTaxCalculator was founded in Sydney in 2018 and has integrated with over 400 exchanges, both decentralized and centralized. They are available in over 20 different countries. This tool is well known for its long list of features that it offers, such as tracking the tax due on not only interest earned via DeFi savings accounts but also airdrops, staking, mining, DeFi staking rewards, and ICO participation!

The company also produces one of the most detailed tax reports, and they support on-chain transactions, the cost of their lowest subscription is $49, but this only supports up to 1000 transactions.

Koinly

The Koinly company was also founded in 2018 and has been integrated into over 300 exchanges. In addition, the company has developed software that is built to provide tax reports and manage and track your crypto assets across exchanges and wallets.

The software’s main feature is the automated data importing ability that allows the user to stay on top of their tax owed as it will update with every new transaction, creating a live tax tracker.

Koinly has offered users the most straightforward package for $49 but does not have a cap on the number of transactions that a user can import.

TokenTax

TokenTax was founded in 2017 and can integrate into all exchanges. The company prides itself on its easy to use software that has simplified the crypto income tax process by allowing users to quickly see their gains but also can utilize a product known as tax-loss harvesting that will tell a user when to strategically sell their losses to offset their tax they are paying on their gains.

The reviews of the products have raved about excellent customer support and the ease of conducting international tax returns.

The product charges a price of $69 for the year for 500 transactions.

Why Income Tax rather than Capital Gains Tax (CGT)

The tax that comes to mind when you likely think of tax and cryptocurrency is capital gains tax (CGT). Capital gains you make from selling an asset for a higher price than you buy it. There are also clauses like a lowered taxable amount depending on how long you own the asset or the class of asset.

This doesn’t apply to interest earned on crypto as the mechanics of how it works are exactly like your traditional bank. Though the technology is new, the way in which you earn the money plus how and when it’s paid out is much more similar to income earned from saving at a bank.

While you can decide for yourself when you want to sell an asset and thus initiate a CGT event, interest earned in a bank is typically accrued daily and paid out monthly. With interest earned in crypto, and especially in the DeFi protocols Minke gives access to, interest is accrued and paid out every few seconds.

Conclusion

So now you know that you’ll likely need to pay income tax on your interest earned from crypto. Hopefully, this article has simplified the concepts and provided some great tools to track your tax obligations. If you’re looking for the best way to save, earn and invest with DeFi then you’re already in the right place – you can use our app Minke to easily earn more interest on your money.

Disclaimer: All advice in this blog is general in nature and does not take into account your individual situation. You should also consult with a tax professional.